John E. Chapman Chief Executive Officer

John E. Chapman Chief Executive OfficerWhile federal estate taxes often grab headlines, many overlook the significant impact of state estate taxes. These state-level taxes can substantially reduce the value of inherited assets, affecting the beneficiaries and the decedent’s legacy.

Illinois, where Clearwater Capital Partners is based, is one of 12 states with an estate tax. It is a uniquely difficult tax to avoid and requires careful planning to minimize.

Illinois Vs. Federal Calculation

You may be familiar with the federal estate tax exemption amount. For 2024, that exemption is $13.61 million, and married couples are generally able to utilize double that amount, meaning the exemption is “portable” between spouses. Any assets above that exemption amount will be subject to the 40% federal tax. For example, a single person passing with $14.61 million would owe $400k, or 40% of the $1 million over the exemption.

Illinois, on the other hand, has an exclusion amount of $4 million. The change from “exemption” to “exclusion” is meaningful here – once you have an estate over that exclusion amount, 100% of the estate is subject to estate tax, not just the amount over $4 million. Another key differentiator from the federal calculation is that the exclusion amount is not portable. For example, a widow with a $5 million estate would still be subject to the $4 million exclusion amount, even if her deceased spouse did not use their personal $4 million exclusion. In this scenario, the projected IL estate tax owed would be about $286k.

Strategies to Avoid Illinois Estate Tax

The fastest way to avoid the IL estate tax is to move out of state. With only 12 states having an estate tax there are plenty to choose from, many of which are also warmer. If you do take this approach, remember that all real property based in IL is still subject to the tax. To illustrate an example: a decedent with a $5 million estate, half of which is in Florida, and half of it is a house in IL, about $143k estate tax will be due, even though the IL assets do not exceed the $4 Million threshold. Refer *here for several other examples of the IL estate tax computation.

2023 Important Notice Regarding Illinois Estate Tax and Fact Sheet

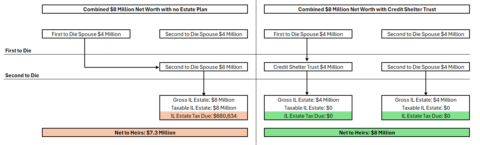

For couples where leaving IL may not be an option, credit shelter trusts can be used to make the IL $4 million exclusion amount somewhat portable. The below chart illustrates how this strategy can assist with avoiding taxes on up to $4 million of assets per spouse.

*The chart above represents a hypothetical situation involving a couple with a combined net worth of $8 Million

The above illustrates how proactively strategizing around the IL estate tax can make it a non-issue, saving hundreds of thousands of dollars.

Final Thoughts

The Illinois estate tax is one of the more complex ones to calculate and avoid. Careful planning and execution are required to prevent paying excess estate taxes. Individuals and families with estates approaching $4 million and even those in the $30+ million family office space need to assess their potential exposure to IL. While the federal estate tax can be minimized using lifetime gifting, a portion of those gifts are clawed back into the decedent’s estate at the time of death when calculating the IL tax due, so a customized state focused strategy is necessary outside of federal planning.

If you would like to discuss your potential estate tax burden and strategies available to avoid some or all of it, reach out to your CCP advisor or the planning team to schedule a meeting.