John E. Chapman Chief Executive Officer

John E. Chapman Chief Executive OfficerOver the past few years, a new kind of financial “advisor” has entered the market, one powered not by experience or judgment, but by algorithms and artificial intelligence. These AI-driven platforms can promise to automate investing, optimize portfolios, and deliver personalized recommendations at a fraction of the cost of a human advisor. While compelling on the surface, these systems operate within predefined parameters and can lack the ability to fully account for personal nuance, emotional behavior, and complex real-world decision-making.

At the same time, the financial services industry has evolved. What was once a transactional client–advisor relationship has increasingly become a personal one. Today’s advisors are expected to understand their clients’ lifestyles, priorities, and long-term goals, and to customize financial strategies accordingly. This shift has raised an important question: how do you quantify the value of an advisor in comparison to what AI can do?

What is the quantitative value of an advisor?

Valuing a financial advisor is inherently challenging because the perceived benefit is subjective and can vary significantly from client to client. Two widely cited studies, Vanguard Advisor’s Alpha and Envestnet Capital Sigma, offer quantitative estimates of the value advisors can add through portfolio construction and asset management. Despite the inherent subjectivity in evaluating advisor value, these two research studies identify three core components of the client–advisor relationship when attempting to quantify the benefit of working with a financial advisor. These three components include Portfolio Construction and Asset Management, Wealth Management and Planning, and lastly, Behavioral Coaching. Together, these areas form the foundation for evaluating the tangible value of an advisor, which this research suggests could amount to as much as 3% per year. To better understand where the estimated 3% of added value originates, it is important to examine each component individually.

What is the quantitative value of Portfolio Construction and Asset Management?

According to Vanguard Advisor’s Alpha, advisors can add approximately 1.04% of added value to a client annually through quantifiable factors such as cost-effective implementation, systematic rebalancing, and tax-efficient asset allocation. However, areas like selecting a suitable asset allocation using broadly diversified funds and a total return focus, versus income investing, are two variables that are incalculable due to the unique facts and circumstances of each client. These areas can be where real value is added as it relates to portfolio construction and asset management.

Similarly, Envestnet Capital Sigma found that portfolio construction and asset management can add 2.43% of added value to a client annually through asset selection and allocation, investment selection using passive management, systematic rebalancing, and tax loss harvesting. Envestnet specifically notes, “a thoughtfully developed asset allocation that is both diversified and consistent with the client’s risk profile and investment objectives can add 0.52% of added value annually”.

However, portfolio construction and asset management are the areas most susceptible to automation. AI systems excel at rules-based portfolio design, cost optimization, systematic rebalancing, and tax-loss harvesting. The competitive advantage for human advisors, therefore, will not rest solely in building portfolios but in integrating those portfolios into a broader financial strategy that accounts for taxes, life transitions, risk tolerance under stress, and long-term behavioral discipline. In this sense, AI may elevate the baseline standard of portfolio management, but it does not eliminate the need for judgment, customization, and accountability.

Taken together, these studies suggest that portfolio construction and asset management represent the baseline value an advisor can provide, possibly resulting in net-even or net-positive value, before accounting for market returns and the other advisory services detailed below.

Wealth Management and Planning

Beyond portfolio management, financial planning can add another layer of advisor value, though it is more difficult to accurately quantify.

Envestnet Capital Sigma states, “The potential added value is difficult to quantify precisely for all subcomponents of financial planning,” but estimates that advisors can add .5% or more in value. Similarly, Vanguard Advisor Alpha highlights that effective spending withdrawal ordering associated with financial planning can add up to 1.20%, depending on the client’s balance sheet and circumstances.

Financial planning encompasses a wide range of objectives, from short-term cash flow needs to retirement income, estate planning, and charitable giving. Since no two clients share the same goals or financial complexity, the value of planning is highly individualized, making precise measurement difficult, but it can ultimately be impactful for clients.

Behavioral Coaching

Behavioral coaching involves helping clients manage emotions and cognitive biases to avoid poor financial decisions, particularly during periods of market volatility. By keeping clients focused on long-term goals rather than short-term market noise, advisors can help prevent costly mistakes such as panic selling or performance chasing. While difficult to measure with precision, Vanguard Advisor’s Alpha estimates that behavioral coaching can add up to 2% of value to a client on an annual basis.

This value is rooted in trust and accountability, elements that technology can struggle to replicate. In many cases, behavioral coaching can represent the single largest source of advisor-added value.

What are all the services a financial advisor provides?

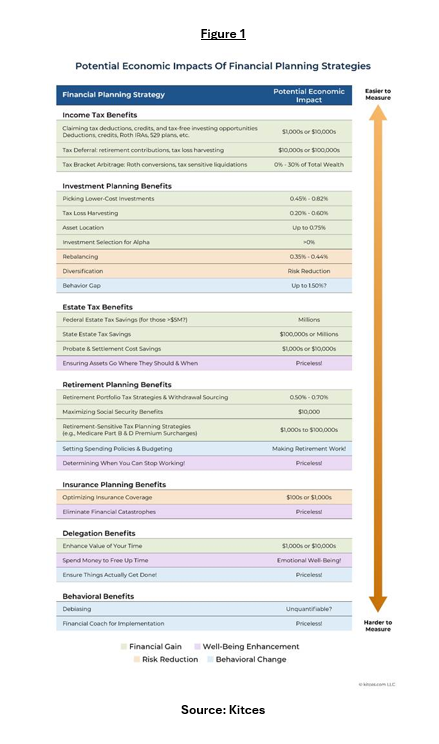

The role of a financial advisor is to help clients make better financial decisions. Under this role, services can include investment management, tax planning and efficiency, risk management, financial planning, retirement planning, estate planning, behavioral coaching, and many “strategic planning” services that relate to the clients’ circumstances. While some of these services are easily visible, others can deliver value quietly and over long periods, making them more difficult to measure.

Figure 1 provides an analysis from Kitces.com, outlining the potential economic value added from the services that a financial advisor can provide. These economic impact estimates include areas not included in the Vanguard Advisor’s Alpha and Envestnet Capital Sigma studies.

Where does AI fall short in Financial Advice?

AI is built upon a set of rules, or parameters, and makes decisions based solely on the information it is given. While this allows AI advisors to efficiently automate investing tasks, it can limit their ability to understand personal context, adapt to life changes, or help guide clients through emotional decision-making during periods of uncertainty. In contrast, human advisors aim to deliver measurable value through customized portfolio construction, comprehensive financial planning, and behavioral coaching, factors that the Vanguard and Envestnet studies suggest can improve long-term financial outcomes by as much as 3%.

The value added by an advisor varies from firm to firm, client to client, and year to year. Rather than replacing human judgment with artificial intelligence, we believe the future of advice lies in empowering advisors with AI – using it to deepen insight, promote increased efficiencies, and help deliver more personalized and disciplined outcomes for clients. The future of wealth management isn’t man versus machine, it’s man empowered by machine.

Connect with Braden Maher to explore more about comprehensive wealth management, alternative investments, and transparent financial advice.

To learn more about Vanguard Advisor’s Alpha and Envestnet Capital Sigma studies, visit their research outputs at:

- Vanguard Advisor’s Alpha: https://www.vanguardsouthamerica.com/content/dam/intl/americas/documents/latam/en/2022/08/mx-sa-2335954-putting-a-value-on-your-value-quantifying-vanguard-advisors-alpha.pdf

- Envestnet Capital Sigma: https://www.envestnet.com/sites/default/files/documents/PMC-CAP-SIGMA.pdf

Author: Braden Maher, Wealth Advisor focused on providing white-glove financial services to clients through financial literacy, honesty, and trust.

Last Updated: February 25, 2026

20260303 – 3