John E. Chapman Chief Executive Officer

John E. Chapman Chief Executive OfficerThe United States and Israeli forces have initiated major combat operations against Iran, explicitly cast as an effort to prevent Tehran from acquiring nuclear weapons and to degrade its missile and naval capabilities. Although it is too early to assess the ultimate duration or disruption of this conflict, the development has already significantly heightened perceived risks to Middle East oil and gas supply and sparked concern over potential Iranian retaliation across the region.

It is entirely natural for investors to worry about the implications of a major military conflict involving the United States. While my strong hope is that these hostilities prove short‑lived and contained, it is still a useful moment to think soberly about how war can shape risk, returns, and the way we set investment strategy.

Please note, this brief note is meant to provide historical context as we contemplate what may lie ahead for capital markets. It can’t, and shouldn’t, attempt to capture the far larger reality: that behind every war are the families displaced, lives cut short, and communities torn apart. The human tragedy and the politics of the current fighting fall outside the scope of this market commentary, but they remain matters of conscience that warrant our own personal reflection.

When viewed through a historical lens, conventional wisdom holds that the primary effects of war on capital markets in the very near term would likely include increased volatility (especially in energy prices), a shift toward risk‑off positioning in global equities, a rotation of capital into perceived safe havens such as U.S. Treasuries, the dollar, and gold, and higher required returns for assets most directly exposed to the conflict.

War should be framed as a volatility event, not an investment thesis. Early‑stage conflicts frequently create sharp, sentiment‑driven moves in equity prices, but the path of markets over the subsequent quarters and years has historically been driven far more by fundamentals like economic growth, inflation, and monetary and fiscal policy than by the conflict itself.

The critical point for investors is that time horizon matters: one‑day or one‑week drawdowns around shock events are common, yet in many past episodes, those declines have been retraced relatively quickly once the initial uncertainty shock is absorbed and markets gain clarity on the scale, duration, and economic implications of the fighting.

Looking back across the major shooting wars of the post‑World War II era, we see the same pattern over and over again: an initial shock, a burst of volatility and price damage over days or weeks, and then a grinding process of repair as markets figure out what is actually at stake and start to fade the worst‑case scenarios.

- First Gulf War (1990–91): U.S. equities weakened into the crisis and then sold off roughly 5–6% over the days surrounding the launch of the air campaign, only to claw back those losses and return to prior levels in about two weeks.

- Iraq War (2003): The S&P 500 dropped a bit more than 5% over roughly a week as combat operations began, then retraced that decline in just over two weeks; over the next 12 months, the index posted strong double‑digit gains as monetary policy, earnings, and growth (not the war itself) came to dominate the tape.

- Russian invasion of Ukraine (2022): The sharpest initial damage showed up in European markets and in countries and sectors closest to the fighting, a classic “geopolitical risk premium,” and yet a meaningful portion of that discount faded over the ensuing weeks as the contours of the conflict and the policy response became clearer.

When you step back from the individual episodes and look at the empirical work on wars and invasions, the picture is consistent: the bulk of the negative equity reaction tends to be concentrated in a tight window around the initial shock and its immediate aftermath. Beyond that event window, returns are increasingly explained by the usual metrics: macro conditions, inflation, interest‑rate policy, and simple geography. War moves markets, but mostly in how it reshapes the distribution of risks at the margin; it rarely rewrites the long‑term script all by itself.

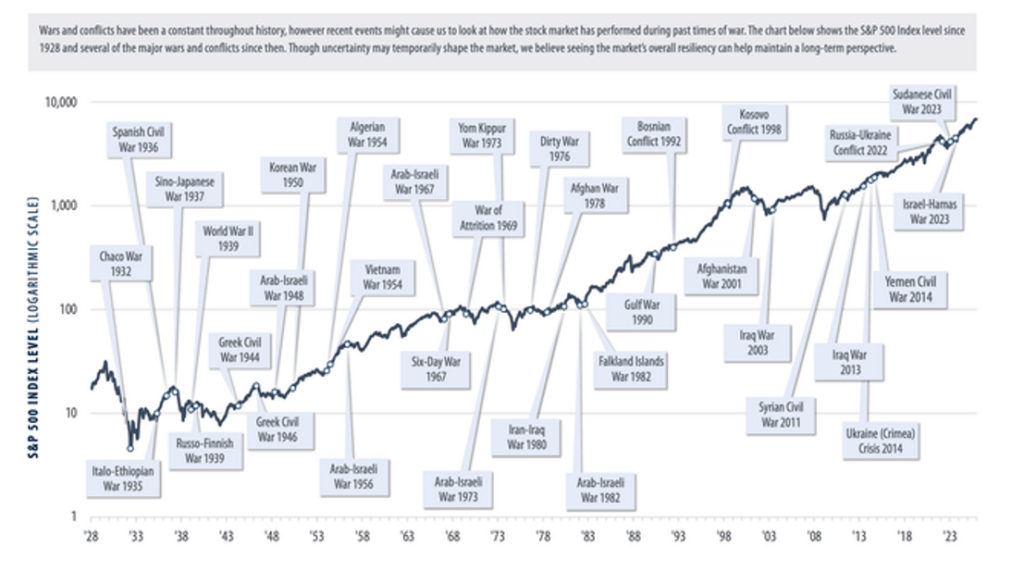

Source: First Trust Advisors

Above is a chart of U.S. equity returns overlaid with wars and conflicts since 1928. It shows repeated bouts of volatility around shocks but a persistent upward trend in cumulative returns over time.

The Pentagon has officially named the current U.S. military operation against Iran “Operation Epic Fury.” In the early, high‑uncertainty phase of the conflict, markets are not trying to “price war” as an abstraction; they are working through a small set of very specific questions.

- The first is duration and scale: are we looking at a contained operation or the opening act of a wider regional conflict that could genuinely dent global growth?

- The second is energy and trade: how much disruption will we see to oil and gas flows, how long might that last, and what does that mean for inflation and, in turn, central‑bank behavior?

- The third is geography: markets ask which economies and sectors are closest to the line of fire, either physically or via supply chains, and therefore deserve a higher risk premium, versus those that sit further away and may prove more insulated.

- Finally, investors weigh the policy response: are fiscal, monetary, and diplomatic actions working to cap the downside tails, or are they making the situation more fragile?

We saw this logic at work during the Russian invasion of Ukraine. European markets and those closest to the conflict bore the brunt of the initial damage, in part because “distance to the war” was a powerful driver of short‑term performance. As the contours of the conflict and the policy response became clearer, much of that geopolitical discount waned.

The broader empirical work tells a similar story: after the initial shock window, differences in market returns are explained less by the existence of war itself and more by familiar forces. This said, given what we currently know about Operation Epic Fury, we would expect to observe some of the following developments in the capital markets over the near term:

- Traditional “risk assets” (such as U.S. equity markets and cryptocurrency markets) should be under pressure as investors process the attacks and weigh the uncertainty ahead.

- Oil companies may benefit from higher oil prices, but gains depend on supply disruptions and infrastructure damage.

- Aerospace and defense stocks may experience an uptick in positive sentiment amid elevated defense budgets.

- Airlines face immediate revenue losses from Middle East airspace closures, and their stocks could experience near term weakness.

- Gold and the United States dollar (USD) are likely to strengthen as investors seek traditional safe havens.

- If Tehran’s response becomes unmeasured or escalatory, the move away from equities and into the safer harbors would likely accelerate.

- Technical support levels will be an important consideration as the conflict evolves.

While disconcerting, geopolitical military conflict does appear to follow a historical pattern. Markets have repeatedly navigated wars and major geopolitical shocks, and disciplined, diversified investors have typically been rewarded for staying invested rather than attempting to time the headlines.

The duration, military impact, and consequences for the region and world stemming from Operation Epic Fury are not known at this point in time. In the end, it’s worth remembering that what we experience as basis points, volatility spikes, and drawdowns on a screen is, in the real world, measured in shattered lives and broken cities. Markets will, in time, do what they always do: reprice risk, discount the future, and eventually move on. The human toll of war is far more complex, and the people impacted by the hostility do not move on so easily.

As this conflict with Iran grinds forward, we at Clearwater Capital have the professional obligation to navigate your capital and investment strategies prudently. We do this while simultaneously recognizing the profound human suffering that sits behind every headline.

History suggests that even from episodes of violence and dislocation, new frameworks, new alliances, and, sometimes, better institutions can emerge. Our hope is that this war ultimately gives way to a more stable regional order, greater security for civilians on all sides, and a world in which the capital we steward is once again deployed primarily toward building, not rebuilding.

Even in the darkest stretches of history, human ingenuity, compassion, and the quiet, stubborn desire to build a better future have always found a way to reassert themselves. We remain confident this will again prove true and that our best days are still ahead of us.

Should you have questions or concerns, please do not hesitate to bring them to the attention of your team at Clearwater Capital Partners.

John E. Chapman

March 2026

20260302 – 1