John E. Chapman Chief Executive Officer

John E. Chapman Chief Executive Officer

One week ago, the United States and Israel began an offensive military campaign aimed at destroying Iran’s nuclear weapons, ambitions, and armed forces capabilities. According to reports, this action has been effective with Iran’s navy, air force, and air defense systems largely eliminated.

Following the onset of hostilities, Clearwater Capital published a short white paper explaining the historical implications of military conflict on capital markets. We described a likely “flight to safety” with monies flowing into traditional safe-haven assets such as the U.S. dollar and gold.

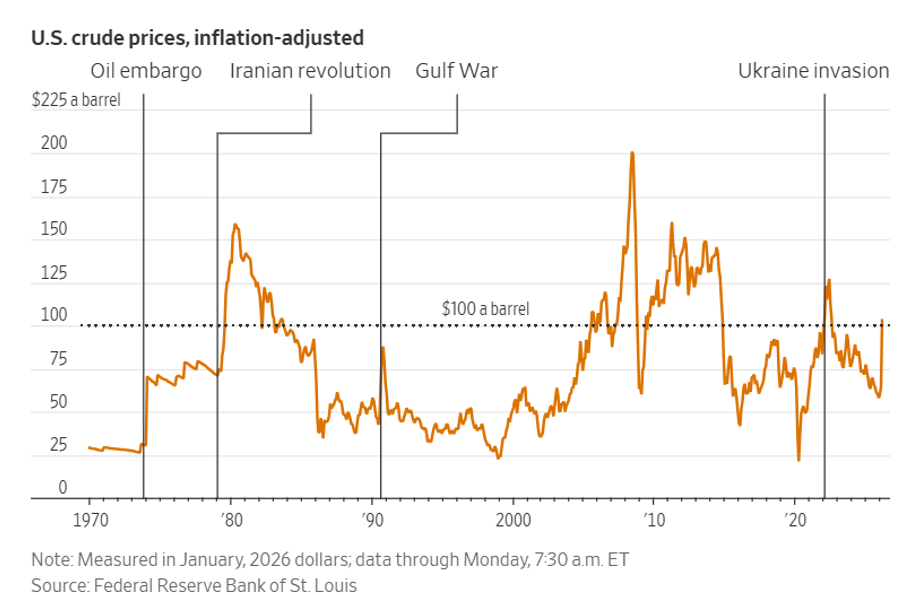

Given the fact pattern of the current conflict, we also set forth the expectation that oil prices were likely to surge, and this morning, the price of oil jumped above $100 a barrel, and U.S. stock prices continued to come under pressure as investors brace for deeper economic fallout from the Iran war.

The price of Brent crude, the global oil benchmark, surged nearly 30% overnight, hitting its highest intraday level since mid-2022. Overnight Asian stock markets slid, with South Korea’s benchmark index down 6% and Japan’s Nikkei 225 falling about 5%. U.S. stocks opened sharply lower as the new trading week began.

In spite of President Trump’s assurances that higher oil prices would fall sharply once the military actions against Iran are concluded, investors appear to fear the energy-price spike could feed inflation and dampen growth, raising the specter of stagflation.

The war in Iran hit equities and other risk assets hard last week. Geopolitical tensions added to investor nervousness about stock market valuations, excesses related to investments in Artificial Intelligence, and emerging problems in the private credit markets. In our commentary last week, we observed that history suggests military conflicts follow a pattern of early shock and volatility lasting days or weeks. The initial burst of volatility should eventually give way to economic fundamentals and government economic policy as fears over worst-case scenarios begin to fade.

Unfortunately, the markets are currently experiencing the early stages of all of these events, and the price damage to risk assets is likely to persist until a clearer picture of the next stages of this conflict begins to emerge. The central question for the markets currently appears to be focused on how much disruption is likely in the energy markets and what it means for inflation, and in turn, central bank monetary policy.

Amid the dominant geopolitical story, the February U.S. employment report continued to stir investor concerns over the strength of the U.S. economy – something we have been writing about consistently in our commentary. Last week’s labor report showed a loss of 92,000 jobs when economists had been expecting a gain of 55,000. The unemployment rate rose to 4.4%.

On the positive side of recent economic reports, it was reported that U.S. productivity rose again, with the average rate of productivity growth over the past three quarters now reaching an annual pace of +4.1%.

We have consistently written about the many distortions and abnormalities of the economic data and trends over the past several years. In many respects, this has been as difficult a period for disciplined investors to navigate as any I can recall in my forty plus years on Wall Street. Now, with the start of a large-scale war in the Middle East, the challenges only escalate.

The key takeaway from all of this is that investors must remain patient, yet vigilant, while avoiding knee-jerk reactions to noisy headlines. There is no case to be made suggesting investors should abandon well-balanced investment strategies. While the evolution of the military conflict is uncertain, we believe the current economic expansion will continue unless we were to see a spiraling in hostilities or an extended closure of the Strait of Hormuz, through which about one-fifth of the world’s daily oil consumption flows. Both of these possibilities appear unlikely at this time.

As we observed last week, history suggests that the outbreak of military conflict only has a temporary impact on capital markets, with “normalcy” returning after a period of shock. Risk assets will remain under pressure until signs of a de-escalation of the war in the Middle East emerge. Until then, investors are encouraged to stay the course, look through the noise, and selectively commit new capital as opportunities present themselves.

Please feel free to reach out to your team at Clearwater Capital Partners should you have any questions or concerns.

John E. Chapman

March 9, 2026

20260309 – 3