John E. Chapman Chief Executive Officer

John E. Chapman Chief Executive OfficerOne of the many provisions emerging from the “One Big Beautiful Bill Act” is a notable addition to the tax-advantaged savings landscape known as a “Trump account”. These new savings vehicles – formerly referred to as “Invest America accounts” and later “MAGA Accounts” – were ultimately codified as “Trump accounts” through the addition of Section 530A of the Internal Revenue Code. Although the Internal Revenue Service has released IRS Notice 2025-68 providing preliminary guidance on certain operational and administrative aspects of these accounts, determining where Trump accounts fit within the broader tax-advantaged savings framework remains an ongoing discussion among industry professionals.

What Are Trump Accounts?

A Trump account is a form of traditional IRA that follows a distinct set of rules during its “growth period,” which begins when the account is established and continues through December 31 of the year before the beneficiary turns 18. On January 1 of the year the beneficiary turns 18, the account transitions from the growth period to what is generally referred to as the “distribution period”. During this time, the account operates under traditional IRA rules.

A beneficiary is considered eligible so long as they will not attain the age of 18 before the close of the calendar year and is a U.S. citizen with a Social Security number. A legal guardian, parent, adult sibling, or grandparent may establish the account on behalf of the beneficiary by attaching Form 4547 to their federal income tax return or by filling out the online form at trumpaccounts.gov. Once created, the individual for whom the account is created is both the beneficiary and the owner.

Key Structural Features

There are five types of contributions that can be made to a Trump account during the growth period:

- IRC Section 6434 pilot program contributions of $1,000 for accounts established for U.S. citizens born between January 1, 2025, and December 31, 2028,

- Contributions from government agencies and charities (referred to as “qualified general contributions”),

- Rollover contributions from a prior Trump account,

- Employer contributions, and

- Standard contributions from family members, friends, and any other party.

Standard contributions are subject to an annual limit of $5,000 while employer-sponsored contributions are further limited to $2,500 per year per employee, both limits indexed for inflation after 2027. Neither standard contributions nor employer-sponsored contributions are permitted prior to July 4, 2026. Unlike traditional IRAs, contributions may be made to the account during the growth period regardless of whether the beneficiary reports an earned income. However, Congress’s omission of language clarifying whether standard contributions will be treated as “present-interest” or “future-interest” gifts suggests that the individual making the contribution may be required to file a federal Gift Tax Return (Form 709). Until further guidance is provided on how such gifts will be characterized for gift tax purposes, individuals should exercise caution when making standard contributions, even if the contribution amount does not exceed the annual gift tax exclusion.

During the growth period, investment options are limited to mutual funds or ETFs that track an index consisting primarily of U.S. companies. Additionally, investments are restricted from using leverage and are required to have annual fees and expenses of 0.1 percent of the balance of the investment, or less. Earnings on the account accumulate free of tax until withdrawn. However, any distribution made during the growth period is generally subject to a ten percent penalty.

How Trump Accounts Compare to Existing Vehicles

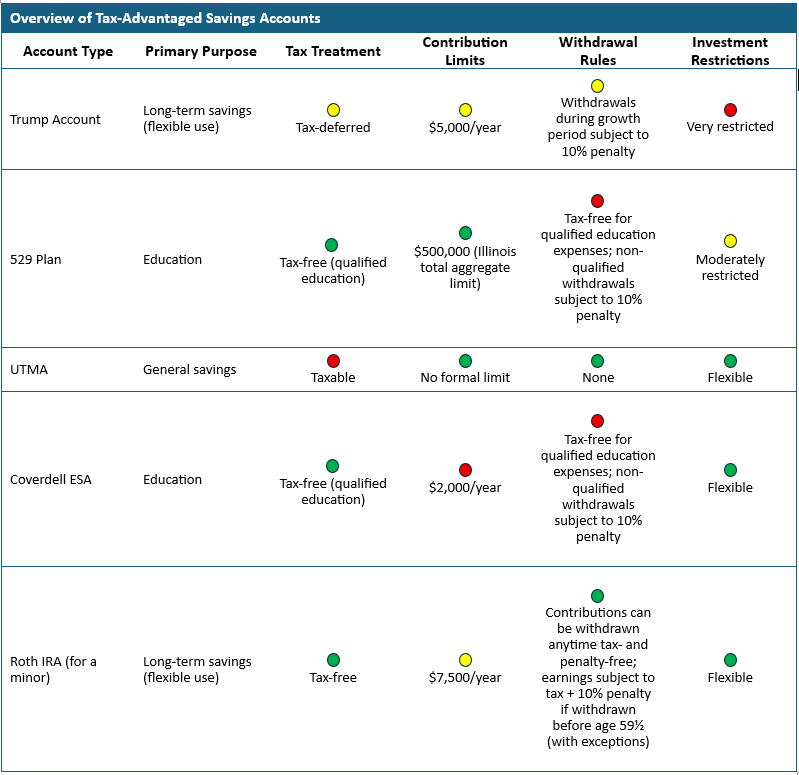

When compared to the other tax-advantaged savings vehicles intended for minors, Trump accounts function as a more restrictive, retirement-style savings option, offering tax-deferred growth and potential government or employer contributions, but with less flexibility than alternatives like Roth IRAs or UTMAs and fewer education-specific tax benefits than 529 plans or Coverdell ESAs. As the role of these accounts begins to take shape, they are frequently viewed as supplemental options within a broader strategy—complementing, rather than replacing, more established tax-advantaged accounts, depending on goals such as education funding, flexibility, or long-term savings discipline.

The table below compares Trump Accounts with existing tax-advantaged savings accounts, including 529 Plan accounts, UTMAs, Coverdell ESAs, and Roth IRAs.

Potential Planning Applications

As practitioners begin to evaluate Trump Accounts, early planning conversations are increasingly focused on how these accounts can be integrated into broader tax-efficient strategies for minors. In particular, advisors may look to coordinate contributions, distributions, and timing of income recognition in a way that creates opportunities for Roth conversions during years when the child is in a relatively low tax bracket. By proactively layering these strategies, Trump Accounts can serve not just as a savings vehicle, but as a planning tool designed to optimize long-term after-tax outcomes.

All in all, Trump accounts may best be viewed as complementary tools, particularly when paired with forward-looking strategies like Roth conversions that can enhance long-term tax efficiency. For families in higher tax brackets, this can involve intentionally realizing income in a child’s name for the sake of converting those dollars into a Roth environment while the child is in a relatively low tax bracket. The result can be a deliberate tax rate arbitrage, where funds are taxed at a lower rate today in exchange for tax-free growth and withdrawals in the future.

This type of planning requires careful coordination with kiddie tax rules, income thresholds, and timing considerations, but when executed properly, it can meaningfully improve after-tax outcomes over time. As a result, Trump accounts may be most beneficial for higher-income households, families already maximizing traditional education savings options, or those seeking flexibility beyond education-specific accounts. When integrated thoughtfully alongside Roth conversion strategies, they can add a powerful layer of long-term, tax-efficient wealth building for the next generation.

Given that legislative and administrative guidance is still developing, families should expect the rules governing these accounts to continue to evolve. If you would like to learn more about how Trump accounts might apply to your specific savings strategy, please get in touch with your advisor or the Clearwater Capital Planning Team.

For more information on Trump Accounts, please visit trumpaccounts.gov. For more tax-related information, please visit irs.gov.

Sources:

- Comparing Education Savings Accounts: https://www.schwab.com/learn/story/comparing-education-savings-accounts

- IRS Notice 2025-68

20260401 – 1